Sign in with Google

Sign in with Google

Key Concepts: Demand, Financial Risk, Rate of Return

Students will be able to:

In this personal finance lesson, students will learn supply and demand by utilizing a system of equations.

Supply and demand is the meat and potatoes of all economic analysis. In this lesson students will get an introduction by creating equations and graphing them to find the equilibrium points. They will have the opportunity to put their Algebra 1 math skills to work in a real world situation by mathematically determining the equilibrium price and quantity using a system of equations.

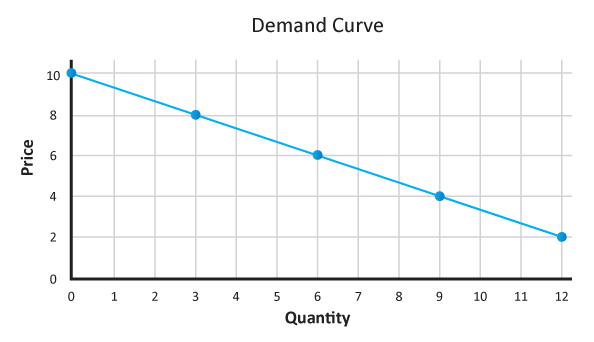

| Price (y axis) | Quantity Demanded (x axis) |

|---|---|

| Price (y axis) | Quantity Demanded (x axis) |

| $10 | 0 |

| $8 | 3 |

| $6 | 6 |

| $4 | 9 |

| $2 | 12 |

As an example, here is a graph of provided data.

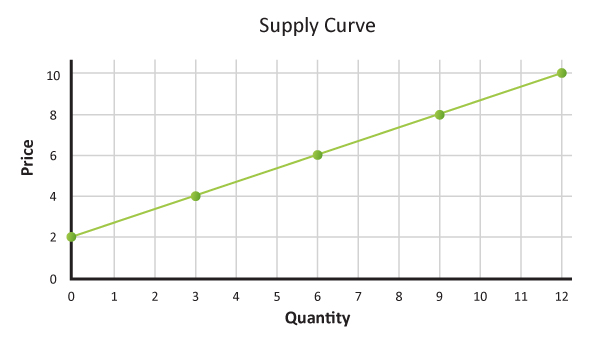

| Price (y axis) | Quantity Supplied (x axis) |

|---|---|

| $10 | 12 |

| $8 | 9 |

| $6 | 6 |

| $4 | 3 |

| $2 | 0 |

Explain that typically as the price of a good or service rises (or falls), the quantity of that good or service producers are willing to produce and sell increases (or decreases).

Ask students to look at the price of $8 on the graph. Discuss the following:

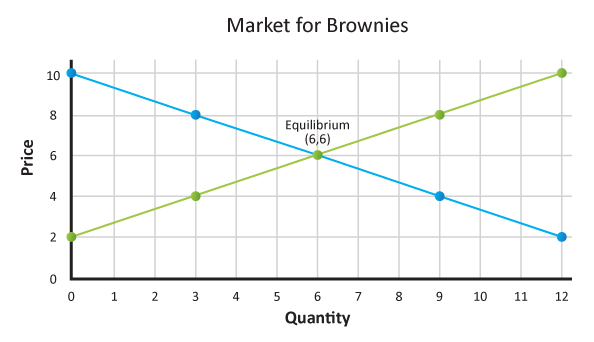

Explain that when the quantity supplied is greater than the quantity demanded, there is a surplus. Ask students what they think will happen that will move the market toward equilibrium; that is, eliminate the surplus. (To sell more of the product, producers will reduce the price. At a lower price, consumers will be willing and able to buy more. This process will continue until the market clears—reaches equilibrium.)

| Price (y axis) |

Quantity demanded (x axis) |

Price (y axis) |

Quantity demanded (x axis) |

| 14 | 60 | 6 | 60 |

| 8 | 120 | 12 | 120 |

| 2 | 180 | 18 | 180 |

Marginal Revolution University

Grades 9-12

Grades 9-12

Grades 9-12